Chipsets known as graphics processing units (GPUs) are perhaps the most important hardware in generative AI development right now. For the last couple of years, investing in semiconductor stocks has generally been a great idea — as you’re nearly guaranteed some form of exposure to GPUs or data centers.

https://theeghumoaps.com/4/8878163

However, 2025 hasn’t gotten off to the best start for chip stocks.

Whether it was drama brought on by Chinese start-up DeepSeek, U.S. President Donald Trump’s new tariffs, or lofty investor expectations, many names in the chip realm haven’t fared so well this year. From a macro perspective, the VanEck Semiconductor ETF has dropped 4% so far in 2025 (as of March 3). When it comes to specific companies, take Nvidia and Advanced Micro Devices, which have seen their stocks decline by 7% and 17%, respectively, so far this year.

While many investors can’t seem to look away from Nvidia or AMD, there’s another stock that’s been caught up in broader selling in the semiconductor landscape — and I think it’s worth buying the dip right now.

Let’s explore why now looks like a lucrative opportunity to buy Taiwan Semiconductor Manufacturing(NYSE: TSM) stock hand over fist.

When it comes to brand recognition in the chip market, investors don’t need to look much further than Nvidia and AMD. These two juggernauts lead the charge in the GPU revolution. Meanwhile, Broadcom plays an integral role in outfitting data centers with advanced chipware, while Micron Technology‘s high bandwidth memory storage solutions are increasingly important as AI data workloads get bigger and more complex.

With so many other names dominating headlines and talking points, I wouldn’t be surprised if you aren’t even aware of Taiwan Semi, or TSMC. The thing is that many leaders in the chip space — including Nvidia, AMD, and Broadcom — should credit Taiwan Semi for much of their success.

TSMC specializes in foundry solutions, which is basically a fancy term that means it actually manufactures chips and integrated systems for semiconductor companies. In other words, without TSMC, Nvidia’s chip architecture would be more of an idea than a tangible product.

Given how much demand there’s been for GPUs over the last couple of years, it shouldn’t come as a surprise that Taiwan Semi’s revenue and profits are soaring. With that said, I think the company’s growth is just beginning to kick into gear.

Many of the “Magnificent Seven” companies, such as Microsoft, Amazon, Alphabet, and Meta Platforms, are exploring custom silicon as a strategy to migrate from an overreliance on Nvidia’s chipware. These big tech giants, as well as ChatGPT maker OpenAI, are reportedly collaborating with TSMC to help bring their visions to life.

Although TSMC has already acquired nearly two-thirds of the foundry market opportunity, I think the advent of more custom silicon — in addition to new architectures from Nvidia and AMD over the next couple of years — will further strengthen the company’s leadership position and lead to a prolonged phase of revenue and profit acceleration.

Image source: Getty Images.

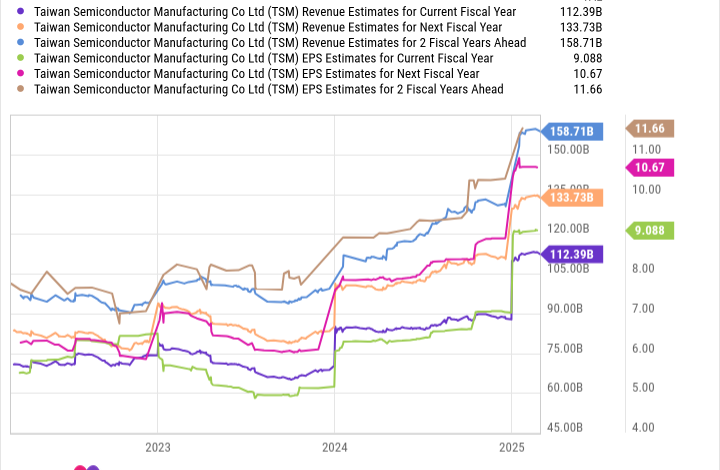

Despite TSMC’s strong market position and robust financial outlook, shares of the chip stock are shockingly cheap.

Right now, the average forward price-to-earnings (P/E) multiple for the S&P 500 is about 21. As the chart above illustrates, Taiwan Semi’s forward P/E is roughly 19. To me, this disparity suggests that investors may see an investment in the S&P 500 as less risky than TSMC — and one that potentially carries more upside, too.

In my eyes, the two main risks revolving around an investment in TSMC are the following:

The semiconductor industry being cyclical.

Geopolitical tensions between China and Taiwan.

While I can understand those points in an academic sense, I think any fears around those topics are overblown. Chip demand isn’t expected to slow down anytime soon, as the market is forecast to increase tenfold over the next decade and reach a size of nearly $1 trillion.

On top of that, TSMC’s operations are not exclusive to Taiwan. In fact, the company just announced in early March that it will be investing an additional $100 billion to expand its manufacturing footprint in the U.S. This seems like a logical decision given big tech is planning to spend more than $300 billion in AI infrastructure in 2025 alone.

I think TSMC stock is a bargain right now. Long-term investors may want to consider buying this stock hand over fist, before the company’s manufacturing operation witnesses even further scale as the AI revolution continues to move full steam ahead.

Before you buy stock in Taiwan Semiconductor Manufacturing, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Taiwan Semiconductor Manufacturing wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $677,631!*

Now, it’s worth notingStock Advisor’s total average return is822% — a market-crushing outperformance compared to166%for the S&P 500. Don’t miss out on the latest top 10 list, available when you joinStock Advisor.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Adam Spatacco has positions in Alphabet, Amazon, Meta Platforms, Microsoft, and Nvidia. The Motley Fool has positions in and recommends Advanced Micro Devices, Alphabet, Amazon, Meta Platforms, Microsoft, Nvidia, and Taiwan Semiconductor Manufacturing. The Motley Fool recommends Broadcom and recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.